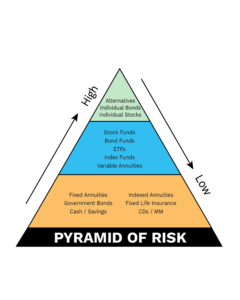

Have you ever heard of The Pyramid of Risk? It helps categorize investments from low-risk (at the bottom of the pyramid) to high-risk (at the top of the pyramid).

Have you ever heard of The Pyramid of Risk? It helps categorize investments from low-risk (at the bottom of the pyramid) to high-risk (at the top of the pyramid).

The bottom of the pyramid includes low-risk investments such as government bonds, fixed and indexed annuities, life insurance, CDs and cash savings. These are considered low-risk investments because they have no direct market volatility exposure.

The middle of the pyramid is for medium-risk investments such as stock funds, bond funds, index funds and variable annuities. These medium-risk investments have market exposure but have more diversified positions than the higher-risk investments.

The top of the pyramid includes alternative investments such as oil and gas. It also includes commodities such as gold and real estate investment trusts. These investments are considered higher risk because they are less diversified and potentially illiquid, meaning you can’t easily get access to your money. Individual stocks and bonds are also categorized as higher risk because of a lack of diversification in highly concentrated holdings. No matter how big or strong one individual company is – as we saw years ago with Lehman Brothers and Enron, companies that many thought were “too big to fail” went bankrupt, or their stock value decreased so significantly that people lost a lot of money.

In the universe of investments, you get to choose what to risk, and when to risk it. Safeguard your money today, risk your purchasing power tomorrow. Risk your money today, safeguard your purchasing power tomorrow. There is no such thing as no risk.

The strength of your retirement plan will be determined by having the appropriate amount of money allocated to low-risk, medium-risk and high-risk investments. The ultimate goal is to create an optimal blend of risk-adjusted investments that will generate predictable income, manage short-term market volatility, and reduce the impact of long-term inflation.